We will update the provisions of TDS for 2082/83 shortly, please visit back after a few hours.

TDS stands for tax deducted at source. Any company or person doing a financial transaction that is subject to TDS payment is required to deduct tax at source i.e while making the transaction. .

The company or person that makes the payment after deducting TDS is called a deductor and the company or person receiving the payment is called the deductee. It is the deductor’s responsibility to deduct TDS before making the payment and deposit the same with the government. TDS is deducted irrespective of the mode of payment–cash, cheque or credit–and is linked to the PAN of the deductor and deducted.

Generally, TDS is deducted on the following types of payments:

- Salaries

- Interest payments by banks

- Commission payments

- Rent payments

- Consultation fees

- Professional fees

- Dividends

- Windfall gains

Here we will be discussing the rates and rules of TDS in Nepal for the FY 2077/2078 (2020/2021).

A. Tax withholding Rates (TDS)

|

S.N |

# Nature of Transaction FY 2020-21 FY 2019-20 |

FY 2077/78 |

FY 2076/77 |

|

i |

Interest income from the deposit under ‘Micro Finance Program’, ‘Rural Development Bank’, ‘Postal Saving Bank & Cooperative (u/s-11(2)) in rural areas is exempted from tax |

No change |

Up to Rs 25,000 |

|

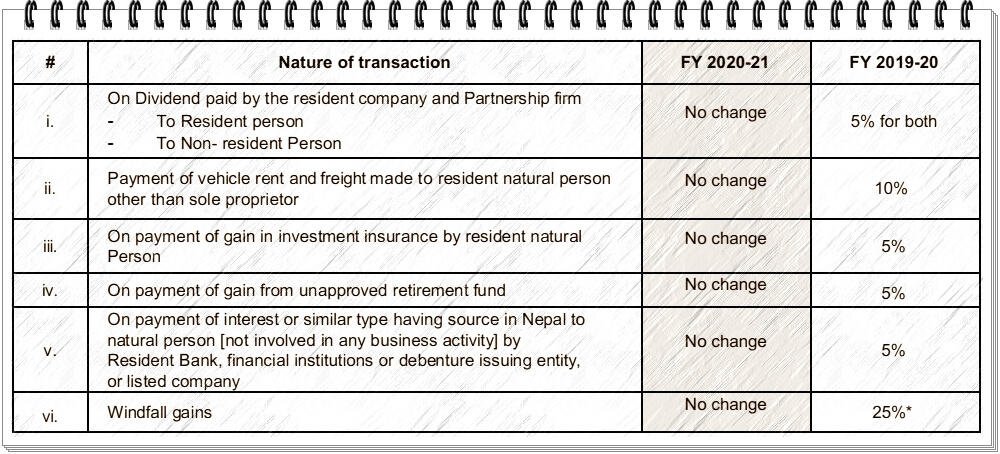

ii |

Windfall gains |

No change |

25%* |

|

iii |

Payment of rent except for house rent to a natural person and except provided in the serial number (iv) & (v) below, made by resident person** |

No change |

10% |

|

iv |

Payment for vehicle hire to VAT-registered person |

No change |

1.5% |

|

v |

Payment for freight or rental payment against the lease of carriage vehicle relating carriage of goods i. Against non VAT invoice ii. Against VAT Invoice |

No change

1.5% |

2.5%

2.5% |

|

vi |

Profit and gain from the transaction of commodity future market |

No change |

10% |

|

vii |

On returns to be distributed by Mutual Fund: – Natural person: Other than Natural Person : |

No change |

5%

15% |

|

viii |

On Dividend paid by the resident company and partnership firm – To Resident person – To Non-resident Person |

No change |

5% for both |

|

ix |

On payment of gain from investment insurance |

No change |

5% |

|

x |

On payment of gain from unapproved retirement fund |

No change |

5% |

|

xi |

On payment of interest or similar type having source in Nepal by Resident Bank, Cooperatives, financial institutions or debenture issuing entity, or listed company – – In case of payment made to natural person [not involved in any business activity]

– In case of payment made to entities |

No change |

5% 15% |

|

xii |

On payment of premium to non- resident insurance company – On payment of commission relating to reinsurance premium to nonresident insurance company |

No change |

1.5% |

|

xiii |

Payment against contract or agreement to Non-Resident person. (Word “repair of aircraft & other contract” removed to include all type of contract or agreement.) |

No change.

|

5% |

|

xiv |

On payment exceeding Rs 5 million made towards the works done through the consumer committee |

No change |

1.5% |

|

xv |

Contract payments exceeding Rs 50,000 |

No change |

1.5% |

|

xvi |

Payment of consultancy fee/ for procurement of services: – – by resident person against VAT invoice – by resident person against Non-VAT invoice |

No change |

1.5% 15% |

|

xvii |

Payment against contract or agreement to Non-Resident person for “repair of aircraft & other contract” removed to include all type of contract or agreement |

No change in rates. |

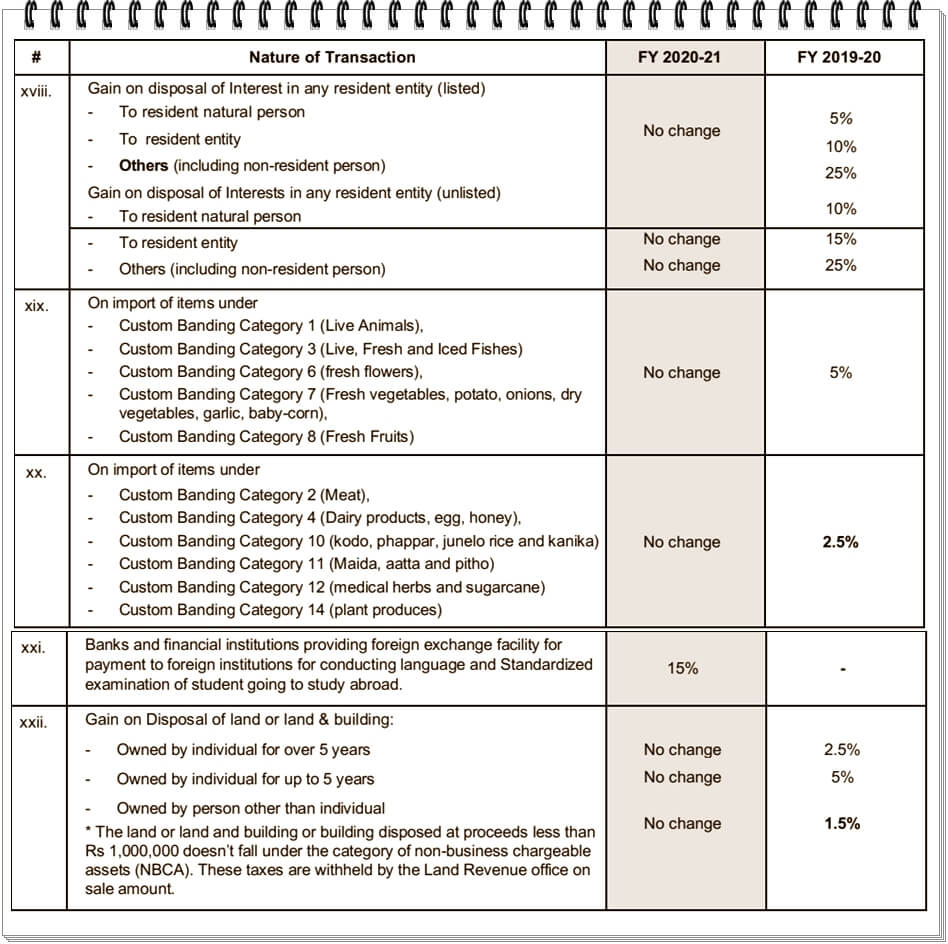

5% |

|

xviii |

On payment for use of Satellite, Bandwidth, Optical fiber, telecommunication equipment or electricity transmission by resident person irrespective of its location |

No change |

10% |

|

xix |

On payment of interest on loan taken from foreign banks in foreign currency for the investment as specified by Nepal Rastra Bank by resident banks and financial institutions. On payment of interest on loan taken from foreign banks for the investment as specified by Nepal Rastra Bank by banks and financial institutions. |

10% |

– |

*Windfall gain tax of 25% will be exempted for the reward up to Rs 500,000 received on behalf of contribution in the field of literature, art, culture, sports, journalism, science and technology and general administration.

B. Rates of Advance Taxes

** In case of house rent other than payment to natural person, additional municipality tax to be included and deposited with the local ward/municipal office (2% in case of Kathmandu and Lalitpur Municipal Authorities)

C. Applicability of TDS

C. Final Withholding Payments

This table contains data of previous years

Only left for reference. The following table contains TDS rates and rules of FY 2076/77. You can simply ignore this.

Tax Deducted at Source (TDS) rates, rules and updates of Nepal for 2073/2074

TDS WITHHOLDING IN OTHER PAYMENTS

S.N |

Nature of Transaction |

2072/2073 |

2073/2074 |

| A | Interest income from deposit up to Rs 10000 under ‘Micro Finance Program’, ‘Rural Development Bank’, ‘Postal Saving Finance Program’, ‘Rural Development Bank’, ‘Postal SavingBank’ & Co-Operative (u/s-11(2) in rural areas) | Exempt from tax | Exempt from tax |

| B | Wind fall gains | 25% | 25% |

| Wind fall gains from Literature, Arts, Culture, Sports, Journalism,Science & Technology and Public Administration amountreceived up to 5 lacs | Nil | Nil | |

| C | Payment of rent by resident person having source in Nepal | 10% | 10% |

| D | Payment of Rent by Resident person having source in Nepal if the Bill raised is VAT bill | 1.50% | 1.50% |

| E | Profit and Gain from Transaction of commodity future market | 10% | 10% |

| F | Profit and Gain from Disposal of Shares: | ||

| In case of Individual | |||

| Listed Shares | 5% | 5% | |

| Non Listed Shares | 10% | 10% | |

| Others | |||

| Listed Shares | 10% | 10% | |

| Non Listed Shares | 15% | 15% | |

| G | On dividend paid by the resident entity. | 5% for both | 5% for both |

| To Resident Person | |||

| To Non Resident Person | |||

| H | On payment of gain in investment insurance | 5% | 5% |

| I | On payment of gain from unapproved retirement fund | 5% | 5% |

| J | On payment of interest or similar type having source in Nepal to natural person [ not involved in any business activity ] by Resident Bank, financial institutions or debenture issuing entity, or listed company |

5% | 5% |

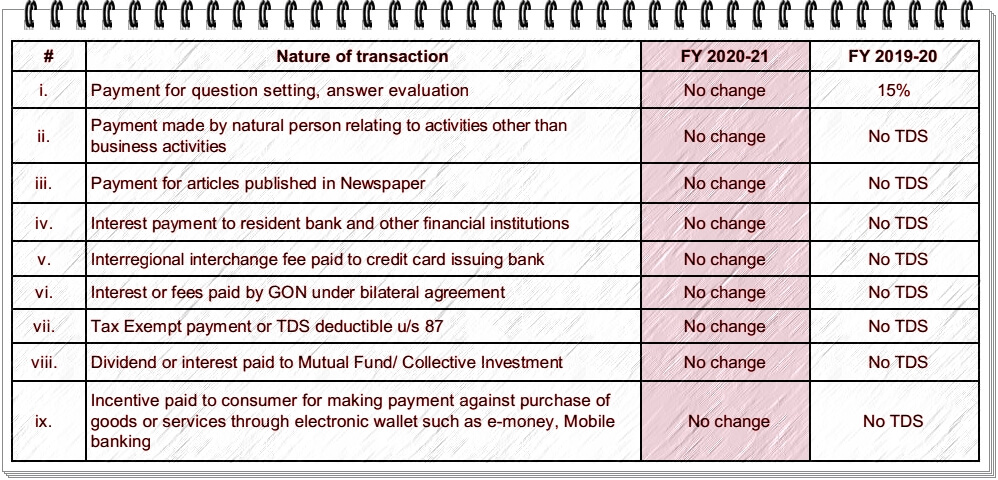

| K | Payment made by natural person relating to business or other payments relating to house rental except house rent | No TDS | No TDS |

| L | Payment for articles published in newspaper, question setting,answer evaluation | No TDS | No TDS |

| M | Interest payment to Resident bank, other financial institutions | No TDS | No TDS |

| N | Interregional interchange fee paid to credit card issuing bank | No TDS | No TDS |

| O | Interest or fees paid by Government of Nepal under bilateral | No TDS | No TDS |

| P | On payment of general insurance premium to resident insurance company | No TDS | No TDS |

| Q | On payment of premium to non-resident insurance company | ||

| R | Contract payment exceeding Rs 50000 for a single contract wtith in 10 days. | 1.50% | 1.50% |

| S | Interest & Dividend paid to Mutual Fund | No TDS | No TDS |

| T | Payment of consultancy fee | ||

| to resident person against VAT invoice | 1.50% | 1.50% | |

| to resident person against non VAT invoice | 15% | 15% | |

| U | Payment on contract to Non Resident Person | ||

| On service contract | 15% | 15% | |

| On repair of aircraft & other contract | 5% | 5% | |

| In cases other than above as directed by IRD. | |||

| V | Gain on disposal of Interest in any resident entity (both listed or unlisted) exchange (Taxable amount is calculated under section 37) | ||

| To resident natural person | 10% | 10% | |

| To others including non resident | 15% | 15% | |

| W | TDS deducted on payment of dividend made by Mutual fund to natural Person is final withholding Tax. | 5% | 5% |

| X | TDS on Payment by Resident Person for utilizing services related with Satellite, Bandwidth, Optical Fiber, equipment relating to telecommunications or electric transmission | 15% | 10% |

| Y | Dividend Paid by Partnership Firm to its Partners | 5% | 5% It is now Final Withholding |

| INCOME FROM INVESTMENT | |||

| S.N | Particulars | 72/73 | 73/74 |

| 1 | INDIVIDUAL | ||

| Tax withholding on capital gain for natural person on transaction exceeding Rs 3 million (to be made by land revenue office at the time of registration) | |||

| disposal of land or land & building owned for more than 5 years up to 10 years | |||

| disposal of land or land & building owned for less than 5 years | |||

| 2 | Corporate | ||

| Income from disposal of non business chargeable assets (Capital Gain) | Normal Rate | Normal Rate (However 10% TDS is deducted by Land Revenue Office) |

OTHER IMPORTANT POINTS FOR TDS IN NEPAL THAT ARE WORTH REMEMBERING

– In case of Disposal of Interest on entity as per section 37 (2Kha), company registrar shall update the register only after receiving the evidence for payment of TDS applicable on capital gain from such disposals. (New)

– Infrastructure tax at the rate of Rs.5/ltr is levied in addition to all applicable taxes on import of petrol, diesel, and aviation fuel. (New)

– Any person and entity licensed to operate casino during the F.Y. 2073/74 shall be liable to pay 30 million rupees as royalty, furthermore, person operating the same business only using modern machines and equipment shall be liable to pay 7.5 million rupees as royalty. (New)

– In case of disposal of land and building by person other than mentioned in section 95(ka), Malpot office during the registration shall collect advance tax equal to 10% of gain on such disposal. (New)

– Presumptive Tax Rates has been changed as follows: (New)

a. Person dealing with Cigarette, Gas etc. and having profit margin up to 3 percent is liable to pay tax at 0.25% of Turnover instead of 0.5% of Turnover.

b. Similarly in case of businesses other than Cigarette, Gas etc. 0.75 percent instead of 1.5 percent of Turnover.

c. In case of Service Industry 2 percent (no Change).

– Natural Person whether Resident or not having Taxable Income exceeding Rs. 40 Lakhs is compulsorily required to submit Income Tax Return within the time limit prescribed by Income Tax Act.

– Person contributing any amount to Prime Minister Relief Fund or National Reconstruction

Fund established by Government of Nepal during any Income Year, are entitled to deduct such amount while calculating taxable income for such Income Year.

I need to know about the rate of TDS on govt. office rent.While asking to others, they are also confusion on either 10% or 15% of monthly rent amount.

Its 12% for local govt…

Dear Sir,

Please confirm the meaning of “other contract” in clause “U” mentioned above is inclusive of the international EPC contract loaned by World Bank under NEA or exclusive ?

I thought that EPC contract should be exlusive, am i right?

Thanking for your kindly reply!

Best regards,

您好张总,您这个问题解决了么?

could you please let me know what will be the taxes to be made from a company. In other words id ABC company ‘s profit is Rs,1000000.00 ( ten lakhs) and if the company’s share holder want s this profit tb divided between themselves as per their shares in the company, whjat percentage of taxes have to bepaid or deucted.

5%

Dear Sir,

I am trying to do a international consultancy as a lead consultant and Have a partner from France whom I awe some percentage of the cost.

I would be grateful to understand if you could help me understand the taxation rules for this. say total project fund is $50000 and I owe the consultant $30000 and I need to send the amount from Nepal.

Thank you

Basudev ji;

The consultancy fee is subject to 15% TDS and 13% reverse VAT. Reverse VAT is which you can adjust with your other business invoice of VAT transaction. You will have to present all your contract with the company along with TDS and reverse VAT submission evidence and present it for NRB approval thru the bank you intend to transact.

Hello sir,

please advise me the penalties on TDS late refiling and how it is calculated .

Do we need to deduct tax for the labor who carry furniture of the office during the relocation of office if yes what rate?

Sir,

I would like to know the TDS on bonus Rate.

KINDLY SUGGEST WHAT IS THE RATE OF BONUS WITH PAN OR WITHOUT PAN IN NEPAL

how much we have time to pay rent tds and salary tds .

Can I please know TDS rate in case of Service import?

13% reverse charge to pe paid and filed during VAT return in addition to the billed amount.

15% TDS to be deducted on the billed amount. Pls note that bank will not make payment unless you provide them the TDS payment challan.

Point (R) says Contract payment exceeding Rs 50000 for a single contract within 10 days 1.5% TDS. Is it applicable if the contract payment is related to service registered in PAN only??

I would like to know is 1.5% TDS applicable on every VAT bill I am confuse.

No.

Only on service-related VAT Bill. You need not deduct TDS on purchase of raw material/stock.

I also confuse of TDs for every vat bill? Please send the inquiry

Dear Sir

Would please tell me if I have to deduct any TDS on Travel allowance and facilitation paymnet?

if an electrician is called to repair telephone line and plumber is called to repair water pipe line, electrician submits pan bill and plumber does not. In such case, how much tax to be levied on such service. Till now, I have treated this kind of service as repair and maintenance wages and has been deducting 1 percent tax. Please, advise.

how to maintain sales scheme tds from dealers? 15% or 25% ?

we provide sales target to dealers then provide gift.

I would like to know is it to deduct 20000 rural tax exemption for less than 1yr or have to deduct the per month rural tax exemption i.e. 1666.66.or how will we adjust the rural tax exemption for less than 1 yr like 6 month, 2 month.

If I am purchasing a software (apparently it will be sent against a pro forma invoice) from outside nepal, what would be the applicable taxes?

Is 15% TDS and 13% reverse vat applicable for this as well, appreciate your comment

hi Ashish ji, so what you did, paid 15%+13%! Some says for software, which is a product, one need to pay only 1.5% TDS and 13% reverse VAT.

if we bye the tally or software. how much TDS Deduct

I THINK 15% TDS WE MUST SUBMIT

For Payment Purpose 15% TDS is to be deducted. However Pro Forma Invoice in itself is not the final Invoice. Only after receiving the Final Invoice can we Book the Expense and Apply 13% Reverse VAT & TDS of 15% can be claimed.

I would like to know that how to make payment of VAT bills by Company after deducting TDS on it.

Example:

VAT applicable amount – 10,000/-

VAT – 13% of 10,000/- = 1,300/-

Total amount – 11,300/-

Option:1

TDS =1.5% of 11,300/- =170/-

Payment =11300-1.5% of 11300 = 11,130/-

or

Option:2

TDS =1.5% of 10000 = 150/-

Payment =11300-150 = 11,150/-

Which one is correct one. Please suggest me

1.5% of taxable amount 1.5% of 10,000/-

Option:2

option 2 is coorect

option 2 is correct.

Option:2

option 2

Option 2 is correct since tds is detucted in taxable amount.

OPTION 2

We are receiving some courier services from india and they have given us invoice as per the law of india

than what would be happen if we are doing payment in Indian currency. what should we have to deduct TDS as per Nepal???

Please answer

Is it compulsory to raise PR, PO for every purchase we made for the project to any amount or is there any minimum value to which PR, PO is no required

If total salary is rs. 1,23,000. how to calculate it’s social security tax and remuneration tax??

is it monthly or yearly income?

If salary of a person is more than 350000 year wise, than it is treated as social security tax moreover the person having salary more than 350000 is tretaed as remuneration incom.

For eg:

salary of Mr Ram: rs 30000 Per Month

year wise salary: 30000*12=360000

First slab – 350000 @ 1% = 3500 ( social security tax)

Next _ 10000 @ 15% = 1500 ( remuneration income Tax )

Dear sir

Please help on a matter. Our company is a resident company in Nepal and we had received transportation and CHA services from a Indian resident comapany and our work contract is more than Rs. 50000/-.

And we want to paid the money to Indian company against his service bill. You are requested please confirm about the TDS applicability??

i want to know TDS rate of heavy repair & maintenance contract with non-resident person/ form.

Could u please tell me what is the tds provision for commission amount?

15%

What is the TDS rate of contractor for the manufacturing of finished goods in an organization.

what is the tds rate for interest income exceeding Rs.10,000.

provision of tds on office rent paid by entity to individual and entity.

I only know following…

1. Deduct 1.5% on Vat

2. Deduct 15% on Pan

Please clarify me following:

1. Is there any difference on deducting tax for service and goods bill?

2. Is there any limit (in bill or Accounting Period) for making applicable TDS rule?

Please clarify me following:

1. Is there any difference on deducting tax for service and goods bill?

2. Is there any limit (in bill or Accounting Period) for making applicable TDS rule?

I would like to get a help regarding TDS on Goods Transport Service:

My company purchases big quantity of coals from the VAT registered vendors for which those vendors issue TAX invoice. However, the coal is transported from vendors’ location to our location by a Third Company which basically deals in transporting such materials and the Third company issues a normal PAN invoice (the amount of invoice ranges from 55K-95K).

Similarly, after the coal reaches our location, we have to pay extra amount for unloading the coal from Trucks.

So, what shall be the TDS implication on these 2 cases?

a) Transportation of Coal from Vendor to our locaiton,

b) Unloading wages paid.

2.5% tds applicable for Goods transport Service

For Transportation of Coal 2.5% TDS should be deducted. For Wages for labor 1% TDS is to be deducted.

what will be the TDS rate for material export from India under a EPC contract for an Indian entity.

Is tds applicable on Transportation & Communication allowance

This will be calculated in Individual’s yearly tax calculation.

Payment made for furniture purchased..what is the rate of tds to be deducted against vat bill

If amount is exceeding Rs. 50k , then 1.5% against VAT bill. If PAN bill was issued then 15% has to be deducted

I am doing a construction contra t in Nepal and Come from India they r deducting 15% TDS how to get refund for the same

Request for the TDS deduction Receipt and verification of TDS deduction at Nepal. You can claim that Tax has already been deducted in Nepal by showing the document when paying you annual tax in India. The amount of tax deduction in Nepal can be deducted from your annual tax payment requirement in India.

Is there any difference on deducting tax for service and goods bill?

The usual practice is that, for service nature we have to deduct TDS. But, for goods bill TDS is not Deducted.

Freight paid to transport of goods by indian to nepal :- mode of transport indian railway or truck by transporter companies is indian company or individual.

question is what about TDS provision……

2nd. in nepal hording bored is revenue expenses or capital expense..

If the freight service is from any foreign nation to custom office of Nepal only then we should not deduct TDS of such nature as the facility received was beyond the boundary of Nepal. If the transportation service is for within Nepal then 2.5% TDS should be deducted irrespective of whether they are registered in VAT or not.

If we purchase goods for the organization and if we have done certain program and we made it from hotel. In that case the amount is nominal we get VAT BILL. So in this case we have to raised tds 1.5% or not.

For TDS of such case on 1.5% TDS of sufficient, since there is VAT Bill.

doesn’t matter whether amount is nominal or not, since hotel or restaurant is VAT registered, you have to deduct 1.5% TDS since hotel provides us restaurant service.

Do we deduct TDS 1.5% or 15% or no TDS on Tea, coffee, food that provided (on request only) by small Khaja Ghar at Government Office.

Dear Sir,

We are EPC contractor from China of NEA, project is loaned by EIB, NEA open LC directly to China for goods which are imported from out of Nepal, so how much TDS will be deducted?

We need to check where the money has been paid, if it has been paid to the Tax bill issued by PE of your company in Nepal then 1.5% , although the Tax invoice has been issued by your PE in Nepal if the amount is been paid directly to your company then NEA shall deduct 5%. Correct me if I am wrong. Thank you !

Why TDS used in collecting income tax?

I am sending money to foreign university through SWIFT money transfer. Do I have to pay TDS?

NO

I found this : (h)Personal services are also tax-exempt. These are services provided, for example, by actors and other entertainers, sportsmen, writers, translators and manpower supplies agents. As it says tax-exempt, then is this means they are also NO TDS services? (It is also written in VAT Act)

Hello sir please help me .

If I am engaged in in a work having the salary of Rs:11,000/- per month what oercent/ amount of TDS shall be paid

Nrs.110 per month. Annually your TDS payment will be 1320.

Generally , 13 months of salary is paid including 1 month of additional payment of Salary in Dashaiin as an allowance . Thus, TDS will be (11000*13)*1%SST = 1430 annually , monthly 119.16

How to pay low tax for the fixed deposit in the bank ?How much tax does need to pay for FD in the bank?

Fixed deposit tax is 5%. Is there anyway we can lower that ?

Can we get the receipt of TDS online in Nepal, that we paid to the government?

TDS on service and fitting charge of electricity and water against pan bill?? is it 10 or 15% ??

15% since PAN bill is issued

tds on allowance?

15%

What is the TDS Rate for The Cargo Companies (International)? Do we have to deduct the TDS on their Service or not?

I am a company if I issue VAT bill to a client for Digital Marketing, what’s the TDS percentage the client should deduct before making the payment??Its 1.5% or 15%?

It will be 1.5%

1.5%

Please Clerify the TDS Deduction on MAterial purchase….. and Vacancy Announcement paid amount

If the company has made contract with suppliers, deduct 1.5% TDS in case of VAT registered and 15% TDS in case of PAN registered. Also Deduct the same TDS as mentioned earlier in case of transactions greater than NPR 50,000 taking it as deemed contract.

For Vacancy Announcement Paid Amount, company shall deduct TDS at the rate of 1.5% as the nature of transactions is supply of service.

https://taxplanetnepal.com/

I am a distributer of abc company FY 2077-78 fy incentives gives to retailers but company dedication 15 % tds to distributer for

Retailers claim amounts but distributer also deposit individual partywise tds 15% amounts to tax office how I claim my company deposit 15 % tds amount

We had a contract for overwheling of Hydroower Electromechanical machine between our company and indian Company and established LC accordingly. But after claim them for payment .

It is applicale VAT and TDS and pls mention the % and payment method.

Can a Service company claim for TDS return or something like that?

Please help me out.

Thank you!

YES IT CAN BE CLAIM

Computer, furniture purchase on vat or pan bill

we deal in selling of automobile parts and lubricants do we need to deduct TDS

Though your business is related to goods which are used for Repair & maintenance, you may receive services and TDS has to be made on services (including Rent, advertisement, contract, etc)

for the advertisement and information of quarterly report ,AGM notice is it same to the news paper article publication or it needs to deduct tax ??

Can I pay my previous years tds in salary this year

i need know about the rate of TDS on govt on Radio brodcating agreement up to five month.

Mero personal vehicle transport ma Use gare vane mero Name ma Company le Payment garda TDS on freight vanera 2.5% katna milxa ki mildaina

I am a company if I issue VAT bill to a client for electronic device or equipment, what is the TDS percentage the client should deduct before making the payment? is it 5%?