Updated Income Tax rates in Nepal for 2079/2080 (2022-23) including tax rates and rules for Individuals and Couples and businesses. The tax threshold slabs for the Fiscal year 2079/80 is updated as per the Budget speech.

All information contained within this document is believed to be correct at the time of publication. While utmost care has been taken in its compilation, no responsibility will be accepted for any inaccuracies, errors or omissions. This publication should not be regarded as offering a complete explanation of any matter contained within it. BizSewa is not responsible for the usage of the information by anyone in any form.

Income Tax Rate In Nepal For Resident Natural person [ Individual (Unmarried) and Married person)] 2079/80 . The table below contains new tax slab in Nepal 2079/80 along with comparason with previous year’s tax rates.

| Tax Banding | Income Tax Rates | Previous Year (For reference) | ||

| Unmarried person | 2022-23 (FY 2079-80) | |||

| (a) Band 1 | First 500,000 | 1%* | First 400,000 | 1%* |

| (b) Band 2 | Next 200,000 | 10% | Next 100,000 | 10% |

| (c) Band 3 | Next 300,000 | 20% | Next 200,000 | 20% |

| (d) Band 4 | Next 10,00,000 | 30% | Next 13,00,000 | 30% |

| (e) Additional Tax | Remaining above 2,000,000 | 36%** | Remaining above 2,000,000 | 36%** |

| Married Person | ||||

| (a) Band 1 | First 600,000 | 1%* | First 450,000 | 1%* |

| (b) Band 2 | Next 200,000 | 10% | Next 100,000 | 10% |

| (c) Band 3 | Next 300,000 | 20% | Next 200,000 | 20% |

| (d) Band 4 | Next 10,00,000 | 30% | Next 1,250,000 | 30% |

| (e) Additional Tax | Remaining above 2,000,000 | 36%** | Remaining above 2,000,000 | 36%** |

*This is the Social Security Tax to be deposited in a separate revenue account (11211) provided for this purpose. However, taxpayers registered as sole proprietorship or on pension income or on income from contribution based pension funds shall not attract social security tax i.e. 1%. And if the taxpayer is depositing an amount in the Social Security Fund (SSF) then for those taxpayers Social Security Tax is not applicable.

** 36 % is computed as 30% plus additional 20% on such tax rate applicable to taxable income above Rs 2,000,000.

To calculate your tax liability add all the personal incomes and check for the slabs to find out rates. For example if you are unmarried and you earn Nrs 8,50,000 per year, your tax is calculated as:

5,00,000*1%=Rs 5000 Plus

2,00,000*10%= Rs. 20000 Plus

1,50,000*20%= Rs 30000

Total Tax= 50,00+20,000+30,000= Nrs . 55,000

Some important notes related to Income Tax rules for resident natural persons.

| A. Deductions in Income | Remarks |

| A natural person working in remote areas entitled to remote area allowance | Additional deduction from taxable amount up to Rs 50,000. (a-50,000, b-40,000, c- 30,000, d-20,000, e-10,000). |

| A natural person with pension income is included in the taxable income. | An additional deduction equal to 25% of the amount prescribed under the first tax band or actual pension receipts, whichever is lower shall be allowed from taxable income. (Note: This provision was removed by Finance Act 2077 and have been reintroduced by Finance Ordinance 2078. |

| Incapacitated natural person | Additional deduction from the taxable amount equal to 50% of the amount prescribed under the first tax band or actual income whichever is lower. |

| B. Reduction on Income | Remarks |

| Life insurance premium | A natural person who has procured life insurance and paid premium amount thereon shall be entitled to a reduction of the actual annual insurance premium or rs 25,000 whichever is lower from taxable income. |

| Medical insurance | A natural person who has insured with a resident insurer/insurance company for health insurance shall be entitled to a reduction of the actual premium paid or rs 20,000 whichever is lower. |

| Insurance of private building (new provision introduced by finance ordinance 2078) | A resident natural person who has insured private building in his/her ownership with resident insurer/insurance company shall be entitled to a deduction of the actual annual premium paid for such insurance or rs 5,000 whichever is lower. |

| Contribution to approved retirement fund | In case of contribution to Social Security Fund (SSF)- 1/3rd of taxable income or Rs 500,000 or Actual contribution whichever is lower.In case of contribution to other approved retirement funds but not in SSF- 1/3rd of taxable income or Rs 300,000 or Actual contribution whichever is lower |

| C. Foreign Allowances | Remarks |

| In the case of the employee employed at the foreign diplomatic mission of Nepal | Only 25% of the foreign allowances are to be included in the income from employment. |

| D. Tax Exemption | Remarks |

| The compensation received against a deceased natural person | The compensation received against the deceased a natural person is not required to be included in income. |

| E. Rebated on tax liability | Remarks |

| Foreign tax credit | If any resident person has paid tax on income outside Nepal, such person can claim the foreign tax credit and while claiming such credit each country has to be considered separately. Amount of credit shall be lower ofi. The total foreign income included in assessable income in Nepal as multiplied by the average rate of tax on total income orii. The actual tax paid in a foreign country |

| Medical Tax Credit | A Resident Natural Person is entitled to Medical Tax Credit at least of the following amount. Rs 750 orii. 15% of Medical Expenses along with any carried forward from the previous year oriii. Actual tax liability |

| Female Tax Credit | In the case of resident individual women having only remuneration income, a tax credit of 10% on the tax liability is calculated as other natural people. I. E., not applicable for women opted as couple status for tax purposes. |

Compulsory Filing

– A natural person with only gains from the disposal of Non-Business Chargeable Assets (NBCA), may opt not to file the income tax return under Section 96.

– Natural person is other than a sole proprietor with income solely from income from vehicle on hire not required to file the income tax return.

– However, a natural person having taxable income exceeding Rs 4 million during an Income Year shall submit income return under Section 96.

Income tax is applicable for Corporations. To calculate the corporate income tax you need to find out the profit after deducting all the allowable expenses and deductibles from the gross profit. Below is the chart of corporate income tax in Nepal for FY 2077/78 (2020-21).

| Source of Income | Tax Rate |

| Normal transactions | 25% |

| Through shipping, air or telecom services, postage, satellite, and optical fiber project | 5% |

| Shipping, air, or telecom services through the territory of Nepal | 2% |

| Repatriation of profit by Foreign Permanent Establishment | 5% |

Corporate Tax Rate 2078/79

| Type of Business | Normal Tax Rate | Rebate | Applicable Tax Rate |

| Normal Business | 25% | – | 25% |

| Special Industry under section 11 for the whole year | 25% | 20% | 20% |

| Constructing and operating ropeway, cable car, railway, tunnel or sky bridge | 25% | 40% | 15% |

| Constructing and operating roads, bridges, tunnel, railway, and airports | 25% | 50% | 12.50% |

| trolley bus or trams | 25% | 40% | 15.00% |

| Entities with export income from a source in Nepal | 25% | 20% | 20% |

| Banks and financial institutions (A, B & C Class) | 30% | – | 30% |

| General Insurance (Non-Life Insurance) | 30% | – | 30% |

| Tobacco, alcohol, cigarette and related products | 30% | – | 30% |

| Telecom and Internet Services | 30% | – | 30% |

| Capital market, Securities, Merchant banking, Commodity futures market, Securities & Commodity broker | 30% | – | 30% |

| Money transfer | 30% | – | 30% |

| Petroleum business under Nepal Petroleum Act, 2040 | 30% | – | 30% |

*above industry-wise applicable tax rate is presented after considering concession available under section 11 of income tax act (ita) except entities falling under tax holiday period. However, in the case of special industry and industry other than presented above, an entity can choose any one tax concession available under section 11 of ita (summarized in point 2.2 below).

**above rebate and applicable tax rates with respect to entities constructing and operating ropeway, cable car, sky bridge, roads, bridges, tunnel, railway, and airports, trolley bus and trams are applicable only up to 10 years from the date of commercial operation.

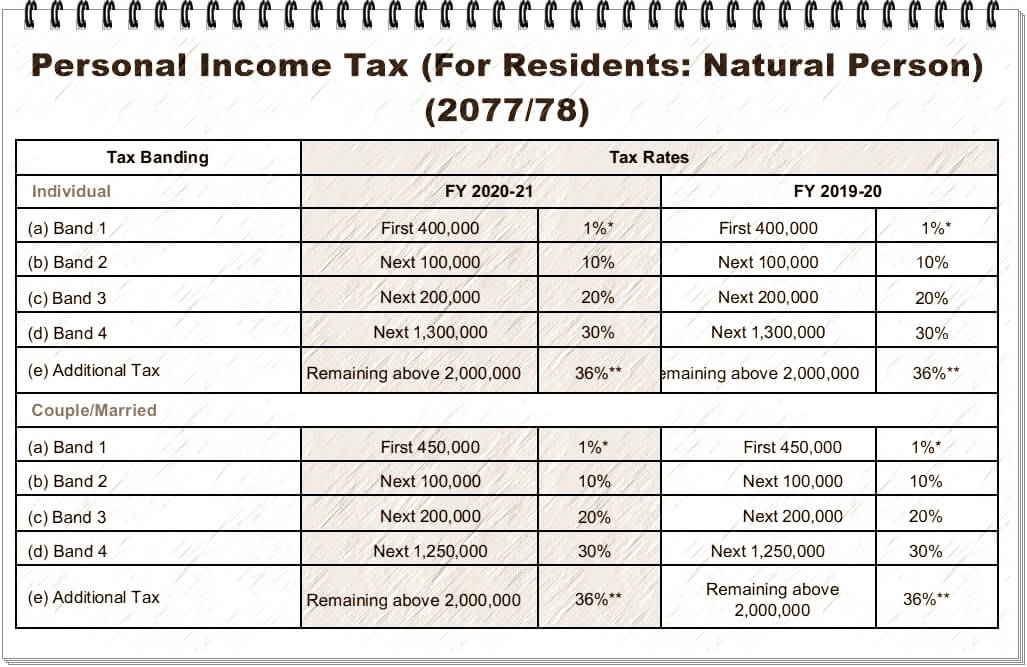

Income Tax rates for F/Y 2077-78 (for reference only)

Tax slab for Resident Natural Person (Individual and married couple). To calculate your tax liability add all the personal incomes and check for the slabs to find out rates.

*This is the Social Security Tax to be deposited in a separate revenue account (11211) provided for this purpose. However, tax payer registered as sole proprietorship or on pension income or on income from contribution based pension fund shall not attract social security tax i.e. 1%. And if the taxpayer is depositing amount in the Social Security Fund (SST) then for those taxpayer Social Security Tax is not applicable

Income tax applicable for Corporations. To calculate the corporate income tax you need to find out the profit after deducting all the allowable expenses and deductables from the gross profit. Below is the chart of corporate income tax in Nepal for FY 2077/78 (2020-21).

By Finance Act 2019-20, tax rates of special industry, entities involved in the operation business of road, bridge, tunnel, ropeway, railway, or sky bridge; operation of trolleybus and tram; export business, construction of infrastructures and construction, production, and distribution of electricity has been removed from the Schedule -1 of the Income Tax Act, 2058. Normal tax rate applicable to the above entities is 25%. However, these entities can avail various concessions given under Section 11 of the Act.

Please check the comment section for discussions and solutions.

Information relevant to previous year (2076/77).

*This information is not updated for FY 2076/77. Please use the facts and figures below for comparisons and referral purpose only.

Notes:

1. Natural person working at remote areas are entitled to get deduction from taxable income to a maximum of Rs. 50000.

2. Natural person with pension income included in the taxable income shall be entitled to deduct from taxable income an additional 25% of the amount prescribed under first tax slab.

3. An incapacitated natural person shall be entitled to get a deduction from taxable income an additional 50% of the amount prescribed under first tax slab.

4. A Resident natural person who has procured life insurance and paid premium amount thereon shall be entitled to a deduction of actual annual insurance premium or Rs. 20000 whichever is less from gross taxable income.

5. A Resident natural person who has procured Health Insurance and paid premium amount thereon shall be entitled to a deduction of actual annual insurance premium or Rs. 20,000 whichever is less from gross taxable income.

6. In case of the employee employed at the foreign diplomatic of Nepal only 25% of the foreign allowances are to be included in the income from salary.

7. In case of the employee posted outside Nepal is getting foreign allowance will get 75% rebate of such allowance.

8. In case of the female employee whose taxable income is only from employment than 10% rebate is allowed on tax liability.

9. In case of individual having income from export, tax rate of 15% is applicable in place of 25%.

10. The limit of 7% of Depreciable Base is not applicable on the repair and improvement expenses incurred for assets located at earthquake affected areas prescribed by GON, in case the person desires to apply this provision. This facility is allowed until FY 2073/74.

11. Productive industries, except tobacco and alcohol industries are eligible to get 50% discount on land registration fee.

12. Special Industries related with manufacturing, tourist services, electricity production and distribution listed on NEPSE and industries mentioned on section 11(3ga) shall be provided with concession of 15% on applicable tax rate. This budget has included Agricultural, Forestry and Mineral Industries also in to the category of Special Industries.

Hy I have my BBS exam of TAX. At exam time do we have imply new tax rate while calculating tax liability?? if we imply old tax rate and calculate tax rate i will get marks or not??

For new course new tax rate have been used for solving tax numerical , if u are new course use the tax rate as your course prescribed otherwise don’t go against the system the course has prescribed for the student. laslty you can’t get marks too.

I’m a past student of Account in Master level.

Hi. I want to know how the 1% SST is calculated , using what formula on excel sheet

Apply the tax rate of fiscal year 2073/74 for currently.

muna tiwari, if you are preparing bbs exam you have to follow the rules of syllabus in which year prepared ie. if you taking exam of 2075 you must follow the rules of tax act of fy 2075/76.

WHAT DO WE CALL THE 1% TAX THAT IS COMPULSORILY DEDUCTED OUT OF ANY LEVEL OF INCOME? BESIDES CALLING IT INCOME TAX, I THINK THERE IS SOME OTHER SPECIFIC TERM USED TO DENOTE IT.

its social security tax

Its Social Security Tax(SST)

it is social security tax.. and it is only applicable to natural persons derriving income from employment to the extent of his employment income….i.e SST for business and investment income is 0

1% tax is termed as Social Security Tax or SST in short form.

Hi ,

i am dk Tumbapo ,

I Have small of Khoisan why much income tax charge in Nepal ,

nothing Devilment Nepal KTM why is very dirty .

but income tax start charge 1% to 35% so why not Devilment Nepal country ,

Ask Devilmaster – Pradeep Dhungana 980100100

our so call Ministers want to collect bigger budget to do nothing,

its development not devilment?????

आयकर कसरी अनलाइन दाखिला गर्ने

VISIT http://www.ird.gov.np

If the annual salary of a married man is say, NPR. 13,00,000/- and also pays for Insurance NPR. 1,00,000/- per annum, how much tax will he have to pay per month? Is there a calculator available online for this?

Hello Lama

You can get tax calculator in IRD website.

In this case, the first thing we need to assess is if the individual’s spouse is in employment else where, and is also paying income tax from the place of employment then the basic exemption limit would be NRS 350000, if not the basic exemption limit would be NRS 400000. Regarding insurance the amount of deduction is the insurance amount paid or 20000 whichever is less. Accordingly, in the above case income tax liability is calculates as follows.

Annual salary 13,00,000

Less:-Insurance 20000

Taxable Salary 1280000

Case 1

Upto 350000 @1% 3500

Next 100000 @15% 10000

Balance 830000 @25% 207500

TOTAL TAX LIABILITY NRS 221000

Case 2

Upto 400000 @1% 4000

Next 100000 @15% 10000

Balance 780000 @25% 195000

TOTAL TAX LIABILITY 209000

REGARDING INCOME TAX CALCULATOR YOU CAN FIND IT IN INLAND REVENUE DEPARTMENT WEBSITE.

THANK YOU,

Dear YAJUSH RAJ POKHAREL Sir,

Your calculation to 15% on 1,00,000 sounds wrong. It should be Rs.15,000 instead of Rs.10000. Isn’t it?

What about both husband and wife earn Rs.4,00,000 per annum each. In total, is the exemption, Rs.8,00,000 for married?

Is it like:

Upto 400000 @1% 4000 (from husband side)

Upto 400000 @1% 4000 (from wife’s side)

Total=Rs.8,000 per year.

Right?

Or like,

Gross Salary of Husband + Gross Salary of Wife =4,00,000 + 4,00,000 = 8,00,000

Upto 400000 @1% 4000

Next 100000 @15% 15000

Balance 300000 @25% 75000

TOTAL TAX LIABILITY NRS 94000

94,000 or 8,000 ???

Tax Liability =90000

Social Security Tax=4000

Above are difference title as per IT Act, So we should be called as Tax Liability=90000 and Social Security tax =4000

Hello Chiranjivee Pokhrel sir , yes my calculation of tax @ 15 % on 100000 is wrong it should be 15000 instead of 10000, pardon me for my typing mistake.

Regarding your other question if both husband and wife are working person then they are assessed as individual and income tax calculation has to be done individually for husband and wife with ceiling limit of 350000 (as per recent tax slab).

Hope this was useful.

Thank you

As per sec 1 (2) of schedule 1 the limit of 400000 is based on the couple option taken as under sec 50 and according to income tax act SST of 1% on 400000 is calculated on total income earned by couple so it is best to use sec 1 (1) instate of taking couple option which will reduce your tax and the main theme of tax is minimum tax is tax thus separate calculation of husband and wife by using the limit of 350000 is done treating them as individual.

well answered.appreciate

I think 9,500.00

Yes, Please contact me.

9849753713

The tax has to be deducted from the basic salary or Gross salary? One married woman’s monthly basic salary is 50,000. Her Dearness allowance is 9500 and communication allowance is 500. Her Monthly Provident Fund is 5000 (10% of basic salary). She is paying 14355 to life insurance. Please tell me how much is her monthly tax calculation that to be deducted from her salary for 7 months until June 2018 (Fiscal year)?

Tax on salary income , i.e Tax deducted at source (TDS) on salary is deducted from the gross salary and not basic salary. Following is the calculation of tax liability (assuming the assessee is assessed as individual)

Basic Salary (50000*7)= 350000

Add:- DEARNESS ALLOWANCE (9500*7) 66500

ADD:-COMMUNICATION ALLOWANCE(500*7) 3500

GROSS ANNUAL SALARY 420000

LESS;-DEDUCTIONS

1. PROVIDENT FUND (5000*7) 35000

2. INSURANCE PREMIUM 14355

NET TAXABLE ANNUAL SALARY 370645

TDS@1% ON FIRST 350000 3500

TDS @ 15% ON 20645 3096.75

GROSS TAX LIABILITY 6596.75

FURTHERMORE THERE IS PROVISION OF 10% REBATE TO FEMALE (ONLY IF ASSESSED AS INDIVIDUAL) ASSESSES ON THE GROSS TAX LIABILITY(6596.75), ACCORDINGLY,

GROSS ANNUAL TAX LIABILITY 6596.75

LESS;- REBATE @ 10% 659.675

NET TAX LIABILITY (ROUNDING OFF TO NEAREST RUPEE) 5937

MONTHLY TDS (5937/7) 848

HOPE THIS IS USEFUL

THANK YOU

Hello sir, can you please reference the source where is this provision of 10% rebate to fermale and from when it was effective from? is this still relevant?

Hello,

Is there a different tax payment rule for part time employees or its the same?

Thank you.

I want to know if employee join a job in the middle of Fiscal year, can we provide fully exemptions for example

staff join on Jan 2017 can we deduct 20000 Insurance premium from his total taxable income, and what would be about exemption of remote allowance

it is irrelevant as to when the employee as joined for new employment. full insurance amount 0f 20000 is allowed as deduction . in case of people working in remote areas there is deduction of upto 50000 from taxable income(after all deductions). the act does not specify anything about remote allowance.

Hello sir can u please provide me your email address

yes u can deduct the full 20000 as insurance premium under zero rated but in case of remote allowances it has a general practice of reducing as per the month basis for eg if worked for 6 month than (remote allowance amt * 6/12)

Please make me clear about INCOME taxes, the income taxes will be deducted from total basic salary or, from gross amount ? like considering below.

food allowance = ?

Remote Allowance = ?

Accommodation allowance = ?

others allowance = ??????

AS PER NEPAL INCOME TAX ACT 2058, TDS ON SALARY INCOME IS ALWAYS CALCULATE ON GROSS SALARY AND NOT BASIC SALARY.

is there ceiling for insurance premium up to 20000? If premium is more than 20000? do we need to pay tax ?

As per fiscal year 2075/76 its limit is 25000 and if it exceed the amount remaining amount is liable for tax

is there any tax rebate for donations paid to temple trust? please help my number is 9864475762 call me and let me know

After staff service retirement services money in nepali upadan rakam amount also we should paid tax to government of nepal.

can female employee enjoy tax rebate on social security tax as well??

No

Hi I want to understand the calculation of Income tax in case an employee leaves the organization after 4 months 15 days of working.

Can we deduct donation for non resident person while calculating taxable income?

HI, Can anyone plz tell me the set off of carry forward and cary backward of losses?

if someone do accounting in any office for specific period like 2 month that while what is tds rate ? can we show as salary and pay tds@1% as SST or not ? what is the tds rate ?

As per sec 87 the total salary that is received in the year is to b calculated and tax is liable on that amount for eg if u work 5 months in one company and 4 month in next and u did not work for 3 months than the total salary is taken on account and what ever is already paid as tax on monthly basis is reduced and exceed amount is to b filed

WHAT THE #### IS THIS??

NEITHER GOVERNMENT DOES WELL NOR LET THE PUBLIC EARN MORE.

#### YOU NEPAL GOVERNMENT.

Yes … I second your thought. This is shit ! Government is literally suckling the blood of citizen. Ir-responsible Fellows !!

Ahely ko house rent ko tax 5% rate ho??

Who do you pay the 5% rent tax ?

A home owner or local corruption district office?

How do the Nepali Government keep records of any individuals income? Isn’t only the government employees and big businesses incomes are reported?

How would Nepali government know how much money farmers or small shopkeepers/ businesses make ?

What about Donation provision?

In case of individual and entity..

As per sec 12 its limit is lower of

100000 or

5% of ATI (adjusted taxable income) or

actual donation paid

this is for both individual and entity

The donation is also given as per sec 12A (sport and heritage protection)

-only for company

-only if donation for infrastructure

-in case of heritage if for repair

condition is lower of following

1000000 or

10% of assessable income

actual amount

and sec 12B (donation to PM relief fund full exemption) for both individual and entity

Is Remittance free from income tax ?

what is details of new INCOME TAX ACCORDING TO 10,20 & 30 % RULE FOR new fiscal year 2075-076?

is this tax rate continues in f.y. 75/76 also?

Swikrit abakas kosh bata ghatauna paune rakam ko upper limit chai kati hola ni ?

Please provide me tax details of Indian employee and employer .

On what kind of expenses TDS is levied. How to know?

where can I find this Provision?

How much tax shall be applied in staff bonus?

Life Insurance premium upto 25,000 is deductible

As per which section of Income Tax Act or Financial Act?? Do you mind quoting the clause??

Can you please mention where is this clause “8. In case of the female employee whose taxable income is only from employment than 10% rebate is allowed on tax liability.”. How can we get such rebate? Being a female, I am eligible for this criteria. If this is really true.

By the amendment of income tax mannal 2073, all female deriving income only from employment is eligible of female tax credit @ 10%.

for more, please go though this link :

http://camunchnepal.com/a-dilemma-over-female-tax-credit-and-its-clarification/

Please explain about TDS in salary and commission!

Hi Good Morning,

My comment is related :

4. A Resident natural person who has procured life insurance and paid premium amount thereon shall be entitled to a deduction of actual annual insurance premium or Rs. 20000 whichever is less from gross taxable income.

: In Fiscal Year 2075/76, Deduction of actual annual insurance premium or Rs.25,000.00 whichever is less form gross taxable income.

Do you mind quoting the section from Income Tax Act or Financial Act?? I couldn’t get the reference for the exact amount Rs.25,000.

आन्तरिक राजस्श्व कार्यलयमा कर बुझाउदा तलबमा लाग्ने १ % सामाजिक सुरक्षा कर र अन्य लाग्ने १०%, २०% र ३६% कर सबै एकै शीर्षक जम्मा गर्दा फरक पर्छ कि पर्दैन ?

पर्ने भए कुन कुन रकम कुन कुन शीर्षकमा जम्मा गर्नु पर्ने हो, सुझाब पाउन।

सामाजिक सुरक्चा मा १% -११२११ मा र

र बाकि सबै पारिश्रमिक कर ११११२ मा

What will be the rental Tax for vehicle hire for NGO

(Red plate and Black plate)

remote ares, please define?

what is the revenue title of tds on freight which we shoul be paid to government of nepal.

what is the revenue title of tds on freight which apply by fy 2075-2076

How about the pension will that be taxed as well?

is festival ( dashain) bonus liable for tax?

yes, it is consider as income from employment under section 8(2) of income tax Act 2058.

what will be the provision for TDS if an employer is not able to pay its staff salaries for some years (say 3 years) and pays all salaries due at end of fourth year, will TDS be levied on each year salary total or total of four years sum as a whole at the time of receiving the salary.

Do Dashain bonus is also calculated in your total annual income and increase your tax slab after receiving Dashain bonus?

I wanna know this too… What they answer you?

Of course included.

What is the tax rate in retirement payment from Government of Nepal?

10% rebate is only for single woman but not married woman right???

suppose you are running a hotel business and your sales revenue is +30 lakh. How to figure the tax liability if the EBT is around 10lakh??

8. In case of the female employee whose taxable income is only from employment than 10% rebate is allowed on tax liability

K Vanna khojeko ho? K yahabaat Sabai Nepali Mahila le 10% discount parcha tax ma???

That mean the female who opt for couple option is not eligible for this rebate.. Others are eligible for this rebate for those whose income is solely based on employment and not any other.

This above provision is further ammended and as per the income tax manual 2073 BS.All the women are eligible for the tax credit of 10% on total tax liability.

Namaskar! is it correct to pay 15% from Upadan amount?

hlw sir i am also bbs third year back student so i forget all terms and condition due to the taxation rules so plzz provide me which have you learn about change in tax rules change ni economic year 2075/2076 plzzz sirr

fixed assets Rs 5K below xa bhane vat bill ma kati % ho and PAN bill ma kati % ?

1.5% on vat 1% on PAN thik ho?

Pasal ma saman kharid garda kti ammount dekhi vat start hunx hola? 1700/ 1800 ammount ko lagi 13 % vat lagaaunu kattiko jayej ho ?

Dear Hira ji

VAT vaneko kati price ma laagne ra kati price ma nalaagne vanne hudain. yo harek goods haru ma impose vaako hunxa… farak yati ho ki tapaai VAT ma register vaako pasal baat saman kinnu hunxa wa VAT ma register navaako pasal baat. VAT vaneko manufacturer baat carry over hudai ultimate consumer ma impose garine tax ho.

Thanks and Regards

Suppose my yearly salary is 480000, how much tax i have to pay.

20 %

Wages ma kati Tax lagxa si

Monthly salary 31500

Festival bonus 30000

Leave enhancement 40000

Plz tax calculation for yearly..

How much sst & 10% tax

Is SST Recoverable?

Hello

IRD.GOV.NP MA LIFE INSURANCE PREMIUM 25000 RAKHDA PANI REMUNERATION TAX ME REBATE MA 20000.00 MATRA DEKHUX.

LIFE INSURANCE PREMIUM 25000 PAY GAREKO X VANE TA 25000.00 SAMMA TAX REBATE HUNE HOINA AS PER ATHIK BIDHEYAK 2075.76

मेरो कुल तलब 672969.6 बर्सिक हुन्छ ।कर्मचारी सन्चय कोष म बर्सिक 71112 जान्छ। मैले जीवन बिम को किस्ता 39781 तिर्छु। मेरो कर नलग्ने बिमा रकम कति हुन्छ । कसैले 20,000 त कसैले 25000 भन्छ कुन ठिक हो?

25000

Features of income tax act 2058 ???

What is the rule for TDS in Nepal? Is it compulsory to pay 15% TDS for the one having total income less than 4 lakhs?

As foreign pensionist volunteering in Nepal I pay tax over my foreign private pension income?

As foreign pensionist volunteering in Nepal I must pay tax over my private foreign pension? will it also depend on the length of stay?

If a Nepali resident receives salary from a foreign company – what rate shall the company deduct the taxes at?

Sir This law is applicable to natural person only. but I want to know about the tax rates applicable to business firm on the basis of their nature of doing business ant the range of their profit..

Can yiu tell me the tax rates for the business firms?

I am now giving BBS third year xm , after lockdown which year’s tax rates must I prefer?

How are CSR expenses treated under TAx

Thankyou for the information . Could you reply please. ? What if i am earning from abroad company sitting here in nepal and i pay tax to the foreign country and then it comes my bank account in nepal . Do i have to still pay income tax on it ?

What is the tax system if couple both are employed? Should they pay tax

from 5 lakhs Or 6 lakh.

your information for income tax is not complete. what about other deductions like medical and life insurance exemption limit, single women natural person rebate limit, under remote area exemption limits, what districts come under A group B group…., disability person 50% rebate is also not clear, give full information with examples .that is helpful…we always expect more extra from any accounting sites than government’s site. thank you.

SST charge on Basic Salary or Earning Salary ? When SSF calculation

Hi I am working in British embassy since 2018 March but I haven’t pay tax because in embassy tax is not deducted in source so that I have to pay my self but I don’t know how pay it.Also I got salary according to english calendar so can u pls suggest me what I can do for it

kalindi construction pvt.ltd

If an employee has salary of Rs. 80,000, has CIT Rs.3,00,000(a year) and insurance premium of Rs. 6,086 (6 months). What will be his\her total salary to be disbursed after tax deduction? Please show the whole procedure of calculation.

For the remuneration tax calculation based on your own figures of earning, other allowance and deductions, you may download the template from https://sites.google.com/view/anykura/excel-kura/excel-files-of-tutorial or watch the video tutorial https://www.youtube.com/watch?v=8UN7EeIqmuY

How many percent of profit distribution tax ?

Hello Sir/Madam,

I would like to know why I am paying Rs.5000 for sole proprietorship firm when i am in loss?

How much tax we should pay if we doing second job

Yes

How will the employer deduct tds i.e. at the slab of individual or couple, for persons opting as couple if the employer is not sure about whether his/her spouse is employed in another company or not ? Can both individuals (husband and wife) take individual benefit of computing tax at the slab of 450000 both opting as a couple in two different companies ?

Married ko yearly income 4 lakh vanda pani less cha vane tax tirnu parcha ki pardaina

parcha. UPTO 4,50,000 1% le tirnu parcha.

eg. if yearly income is 200,000 then tax = 200,000*1% i.e 2,000/-

& if yearly income is 500,000 then tax= (450,000*1%) + (50,000*10%) i.e 9,500/-

source of income salary ho vanne 1% tirnu parxa

I want to know more about taxation policy of nepal in fy.2077/78

i want to know legal information for agriculture firm and want to know if the income is taxable

Tds salary bat factory ma katdain vane ke huna6

Yes

अपांगता परिचय पत्र भएको कर्मचारीले कति प्रतिशत Tax छुट पाउछ होला ? अन्य छुटहरु र सहुलियत के के छन् ?

**

as updated, the Insurance amount is 40K not 25K.

I work as part time lecturer in a college. I don’t have any other income source and I am married and my income is below 500000 annually. What is the tax rate in current government provision. I came to know 15% tax rate for part timer even though it falls in the 1% slab as the new budget rule for employees. Is it correct? and is it fair for the part timer to pay such high tax.

Sunil gautam jii. I have the same problem. What have you been doing till now ? Do i have to pay 15%

Ma India bata afai saman lerayera ghar ma nai online business garna la but it’s a small clothing business only to support my family how much I need to pay tax ?

in nepali language?

i want in nepali laguage.

There is on query regarding taxes on leave . For example i have 60 days accumulated leave in an organization while i resigned and at the time of clearance in what percentage tax deduction are allowed

What is the income tax rate for a company which exports software or provides BPO service to foreign company ?

how much tax should be pay on gratuty fund return ?

Hi sir

I am from India but I am doing accounting for Nepal company

I want to ask if we have deposited tds of salary upto 5/6lakh in Remuneration tax and salary above 6 lakh in social security tax

Can it be adjusted with each other.

Please reply 🙏

If I working two different company then how to calculate my tax??? My salary is 25000 and 45000 …

Great Article

Married Manager joined the company with salary of 90thousand from Magh 1st 2080. aba salary tax calculate garda usko paileko income herne ki naherne? ki just 1% katdine?? please help this issue